Blockchain Payments: A Comprehensive Guide

Discover how blockchain payments are transforming the way businesses accept and move money worldwide.

- Remove the current class from the content27_link item as Webflows native current state will automatically be applied.

- To add interactions which automatically expand and collapse sections in the table of contents select the content27_h-trigger element, add an element trigger and select Mouse click (tap)

- For the 1st click select the custom animation Content 27 table of contents [Expand] and for the 2nd click select the custom animation Content 27 table of contents [Collapse].

- In the Trigger Settings, deselect all checkboxes other than Desktop and above. This disables the interaction on tablet and below to prevent bugs when scrolling.

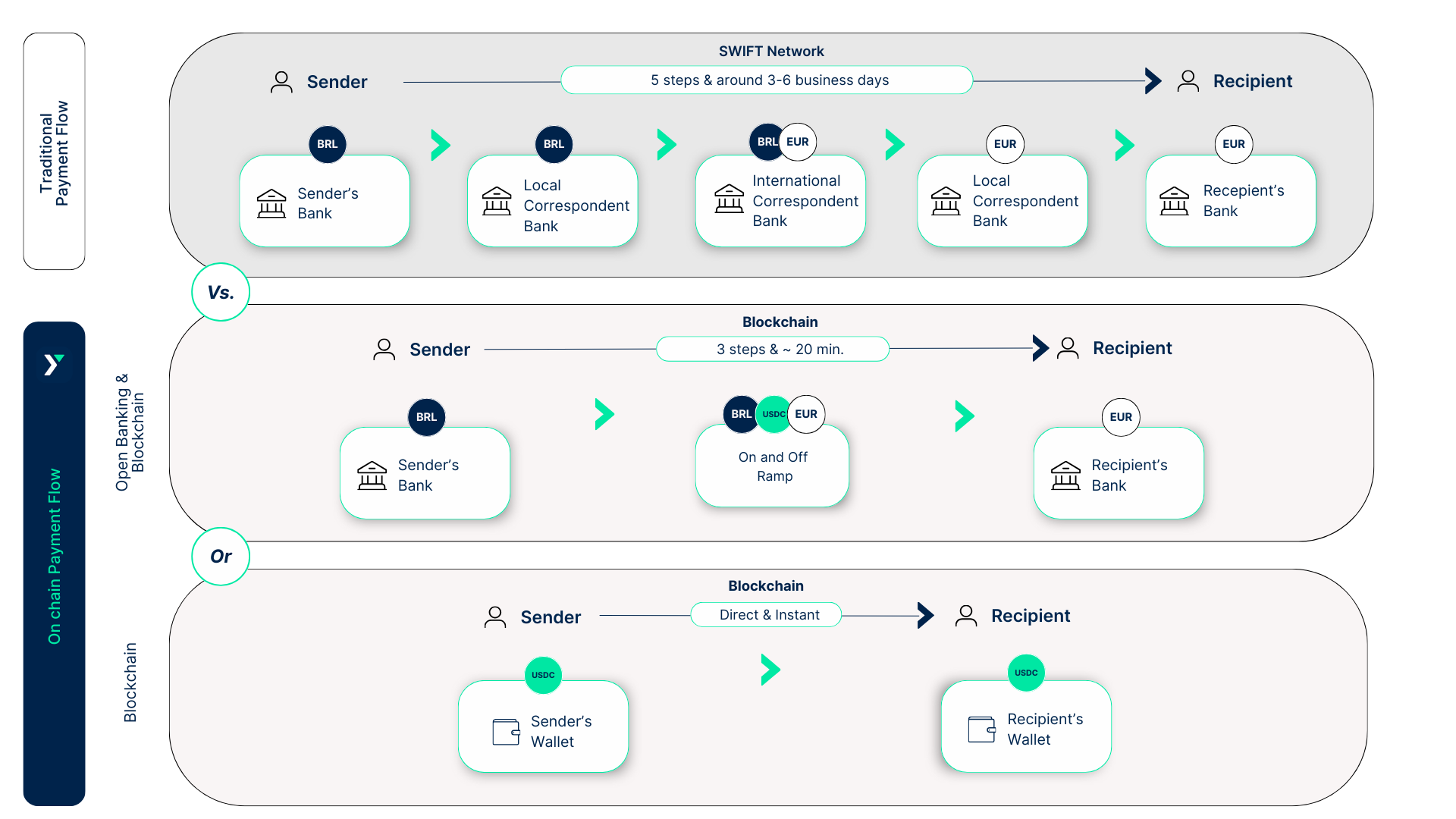

Money still moves the way it did decades ago: through layered networks, fixed processing windows, and a long chain of intermediaries that each add fees and friction. Blockchain payments introduce a different set of rails, ones that run continuously and can settle value directly between parties with a shared record of what happened.

For global businesses, that shift is less about novelty and more about options. When customers, contractors, subsidiaries, and suppliers are spread across time zones and banking regimes, the ability to move value quickly, predictably, and with clear traceability can change how cash management feels day to day.

What a blockchain payment is, in business terms

A blockchain payment is a transfer of a digital asset (often a cryptocurrency or stablecoin) from one wallet to another, recorded on a distributed ledger that multiple computers maintain together. Instead of relying on a bank, card network, or clearinghouse to confirm and reconcile the transaction, the network itself validates it through cryptography and consensus rules.

Once confirmed, the payment becomes part of the ledger’s history. That permanence is the point: the ledger is designed to be very hard to alter, and verification does not depend on a single institution.

How blockchain payments actually work

At the operational level, the flow is straightforward even though the underlying infrastructure is new.

A payer creates a transaction in a wallet and signs it using cryptographic keys. That signed transaction is broadcast to the network. Validators (or miners, depending on the blockchain) check that the transaction follows the rules, including that the funds exist and have not already been spent. When the network reaches agreement, the transaction is added to a block and the recipient’s wallet balance updates.

Settlement timing depends on the chain and the asset used. Some networks confirm in seconds, others in minutes. Many run 24/7, including weekends and holidays, which is a meaningful difference from bank cutoffs and batch processing.

The main types of blockchain payment systems

Not all blockchain payments behave the same way. The asset you accept (and the network it moves on) determines volatility, speed, cost, and the kind of customer experience you can realistically support.

Cryptocurrencies

Bitcoin and Ether are the most recognized examples. They can work well when customers already hold them and want to pay directly without involving traditional banking rails.

They also introduce a pricing challenge: the value can move materially between checkout and conversion to fiat, and that affects margins unless you hedge or convert immediately.

Stablecoins

Stablecoins aim to keep a steady value by being pegged to an asset, most commonly a fiat currency like the US dollar. Many businesses gravitate toward stablecoins because they preserve much of what is attractive about blockchain rails (speed, availability, global reach) while reducing the day-to-day volatility problem.

If your goal is “digital dollars that move like the internet,” stablecoins are usually the first place teams start.

Central bank digital currencies (CBDCs)

CBDCs are digital forms of sovereign currency issued by central banks. Some designs may use distributed ledger technology; others may not. What matters for businesses is that CBDCs would combine fiat stability with faster, more programmable settlement, but broad access and international interoperability are still limited in most regions.

They are promising, but planning your payments stack around CBDCs today is usually premature unless you operate in a market where a live CBDC is already relevant.

Layer 2 networks

Layer 2 networks sit on top of base blockchains and aim to reduce fees and increase throughput. They can make small, frequent payments practical by moving activity off the main chain while still anchoring security back to it.

For commerce, Layer 2 often shows up as a better customer experience: faster confirmations and lower network fees during busy periods.

Quick comparison table

Why global businesses consider blockchain rails

Blockchain payments can be useful even when you keep your unit economics and accounting firmly anchored in fiat. The value tends to show up in settlement behavior, cross-border efficiency, and new workflow possibilities.

After a typical operational paragraph like the one above, the benefits are easiest to scan in a compact list:

- Faster settlement windows

- 24/7 payment availability

- Reduced intermediary layering

- Finality: confirmed transfers are effectively irreversible on-chain

- Auditability: time-stamped records can be verified independently

- Programmability: payments can be tied to logic via smart contracts

Faster settlement and availability

In many traditional cross-border flows, “paid” and “settled” are two different moments. Blockchain networks compress that gap. When settlement speed improves, treasury teams gain cleaner cash visibility and can reduce the operational buffers that creep into forecasting.

This matters most when you pay suppliers across regions, move funds between entities, or run marketplaces where payout timing affects retention.

Lower costs, especially across borders

Intermediaries add both explicit fees and hidden spreads. Blockchain networks still have fees, and they can rise during congestion, but businesses often find that stablecoin transfers on suitable networks are cost-competitive relative to international wires and other cross-border methods.

Cost is rarely just “fee per transaction.” It is also the time spent tracing payments, resolving exceptions, and reconciling records across multiple institutions.

Finality, security, and the operational reality

Finality is a double-edged feature. On one side, it can reduce chargeback exposure and certain fraud vectors that rely on reversals. On the other side, a mistaken address or compromised credentials can mean funds are gone with no built-in undo.

Treat blockchain payments as a different risk model, not a risk-free one.

Transparency and auditability

Public blockchains provide a shared transaction history that can be inspected by anyone. Permissioned systems can restrict that visibility while retaining a consistent ledger model.

For finance operations, the practical advantage is simpler traceability: payment time, amount, and destination are recorded in a uniform format that does not depend on a bank statement arriving later.

Programmability: money as workflow

Some networks support smart contracts, which are pieces of code that execute when conditions are met. That can translate into real business workflow improvements: escrow that releases on delivery confirmation, automatic revenue splits for creators, or usage-based billing that settles in smaller increments.

A programmable payment is not only a transfer. It can be a control mechanism.

Ways to accept blockchain payments

The right integration approach depends on what you are optimizing for: speed to launch, custody control, volatility exposure, or customer reach.

Before choosing a model, it helps to clarify what “accepting” means inside your organization. Do you want to hold digital assets? Do you only want the rails but prefer fiat settlement? Are you solving for checkout conversion, supplier payments, or both?

A short checklist keeps the conversation grounded:

- Asset scope: which coins or tokens you will support, and why

- Conversion plan: whether receipts are held, periodically converted, or converted immediately

- Customer experience: QR codes, payment time limits, confirmation handling

- Compliance posture: KYC/AML expectations across jurisdictions you serve

Direct acceptance

Direct acceptance means you generate and display wallet addresses (often as QR codes) and receive funds into wallets you control. You gain maximum control and potentially lower processor fees, but you also take on key management, monitoring, and operational security.

This route fits teams that already have strong security practices and want custody control as part of treasury strategy.

Using a payment processor or gateway

A processor can handle the on-chain complexity and settle to your preferred currency. That usually simplifies volatility management and reduces the internal workload around blockchain monitoring and wallet safety.

It also helps keep the checkout experience familiar for customers who do not want to think about networks, gas fees, or confirmation counts.

Stablecoin-only acceptance

Some businesses limit acceptance to stablecoins to keep pricing and accounting closer to fiat. In cross-border settings, stablecoins can behave like a fast-moving digital dollar while still landing on blockchain rails.

The trade-off is customer choice: crypto holders who only want to pay in Bitcoin or Ether may drop off if stablecoins are the only option.

Hybrid or custom integrations

Hybrid approaches show up when businesses serve multiple audiences or run multiple flows, like consumer checkout plus supplier payouts. You might accept stablecoins for most payments, offer a limited set of cryptocurrencies for demand coverage, and route settlement differently based on region or transaction size.

Hybrid models are flexible, but they require crisp operational rules so finance, support, and risk teams stay aligned.

The biggest challenges to plan for

Blockchain payments can work well, but they reward careful design. The friction is rarely in “sending value” and more often in everything around it: pricing, customer support, compliance, and incident response.

After establishing that context, the main challenges can be framed clearly:

- Price volatility (mainly for non-stable assets)

- Network congestion and variable fees

- User error risk: wrong address or wrong network can be irreversible

- Regulatory uncertainty: rules vary widely across jurisdictions

- Security posture: custody, key management, and operational controls

Volatility and treasury exposure

If you accept volatile assets, define who owns the price risk and for how long. Even a short time window between payment and conversion can introduce unexpected variance in revenue.

Stablecoins reduce this problem, though stablecoin risk shifts toward issuer quality, reserve practices, and regulatory treatment.

Congestion, fees, and network choice

Popular networks can become expensive or slow during peak demand. Layer 2 networks and alternate chains can relieve this, but you will need policies that determine which networks you support and how you communicate that choice to customers.

User experience and support load

Wallet-based payments ask customers to do more: pick a network, approve a transaction, and wait for confirmation. Businesses that succeed here usually invest in clear UI prompts, QR-based flows, and support processes that can quickly diagnose “sent but not received” cases.

Regulation and compliance

Compliance is not optional, and it is not uniform. KYC/AML expectations, reporting requirements, and restrictions on specific assets or services can differ substantially by country.

Many businesses reduce operational risk by working with licensed providers and keeping internal policies explicit about supported geographies and use cases.

Security and irreversibility

Blockchains are resistant to ledger tampering, but wallets and endpoints are still targets. Internal controls matter: access management, approval workflows, secure storage, and incident playbooks.

Finality is powerful when you want certainty. It is unforgiving when your process is loose.

What Yugo Brings to Blockchain Payments

Stablecoins are often the first practical entry point into blockchain payments. They combine the speed and availability of blockchain rails with the price stability businesses need for accounting, pricing, and treasury. Yugo starts there, but goes further by turning stablecoin payments into part of a complete, multi-rail payment infrastructure designed for real-world operations.

From Stablecoin Acceptance to Payment Orchestration

Yugo enables businesses to accept stablecoin payments while avoiding the operational burden that typically comes with blockchain adoption. Stablecoins can be received, converted, or settled alongside fiat flows without friction.

From that foundation, Yugo orchestrates the most efficient rail for every transaction, whether that is a stablecoin transfer, a bank A2A payment, a card transaction, or a local payment method: through a single API.

Always-On Settlement, Designed for Business

Blockchain rails remove banking cutoffs. Yugo leverages stablecoins to enable near-instant, 24/7 settlement across borders, including weekends and holidays. Funds move faster, cash positions become clearer, and treasury teams gain predictability without relying on correspondent banking chains.

Cost Efficiency Without Operational Trade-Offs

By routing payments intelligently across rails, Yugo reduces unnecessary intermediaries, FX spreads, and processing fees. Stablecoins are used where they deliver clear economic advantage; traditional rails remain available where they are more suitable. The result is lower total payment cost without sacrificing reach, reliability, or compliance.

Programmable Payments as a Control Layer

Yugo brings blockchain programmability into everyday payment flows. Payments can follow logic-conditional releases, automated allocations, or escrow-style holds, while remaining fully auditable and operationally governed. Money becomes part of workflow automation, not just a settlement event.

Compliance-First Blockchain Adoption

Yugo abstracts blockchain complexity while embedding compliance into the payment layer. Transaction monitoring, governance controls, and regulatory readiness are built in, allowing businesses to scale stablecoin usage safely alongside fiat payments. Blockchain rails operate within a controlled, enterprise-grade framework, not outside it.

One Integration, Full Visibility

All flows-stablecoin and fiat are unified into a single ledger with real-time reporting and simplified reconciliation. Finance and operations teams gain one source of truth across rails, currencies, and regions, turning blockchain payments into a transparent, manageable part of the broader payments stack.

With Yugo, stablecoins are not an isolated feature. They are the starting point for a smarter, multi-rail approach to global payments, one that combines blockchain speed with traditional reliability, and turns new rails into measurable business advantage.